Federated Hermes: Navigating competing definitions of the lower mid-market

In the absence of consensus on what the lower mid-market is, investors are approaching this segment of private equity with vastly differing approaches that lead to vastly different outcomes.

By Brooks Harrington, CIO, Federated Hermes Private Equity

As private equity continues to mature – surpassing $ 5 trillion in assets in 20251 – and the returns that investors saw a decade ago become increasingly difficult to replicate today, more investors are moving down the market in search of a better return.

Against this backdrop, the term ‘lower mid-market’ is widely used to describe a vast – yet undefined – range of companies at the smaller end of the scale. It is here that, we believe, many of the industry’s most exciting opportunities reside.

However, in the absence of any consensus, investors are approaching this segment with vastly differing views of what the lower midmarket is. Depending on who you ask, the segment can include companies with an enterprise value of up to $ 500 million, while in some cases, companies with a value as high as $ 2 billion are also being described as lower mid-market.

We take a narrower view, defining the lower midmarket as private equity portfolios with a median enterprise value of up to $ 500 million. In practice, however, our investment strategy focuses on the smaller end of that range. In the fifth vintage2 of our co-investment program, the median enterprise value of the 45 companies we backed was approximately $ 140 million.

Across this segment, we believe there is a large opportunity set of healthy, growth-oriented businesses well-positioned to benefit from the professionalisation and commercialisation that institutional investors can provide. These companies are also typically absent from most limited partner portfolios.

Opportunities in an imbalanced industry

Historically, private equity inflows have aggregated at the mid and upper end of the market where many LPs are now fully invested. However, a sluggish exit environment along with a sharp slowdown in asset growth has left many investors waiting longer than average to realise a return.

Constructing a lower mid-market portfolio requires specialised knowledge and an established network.

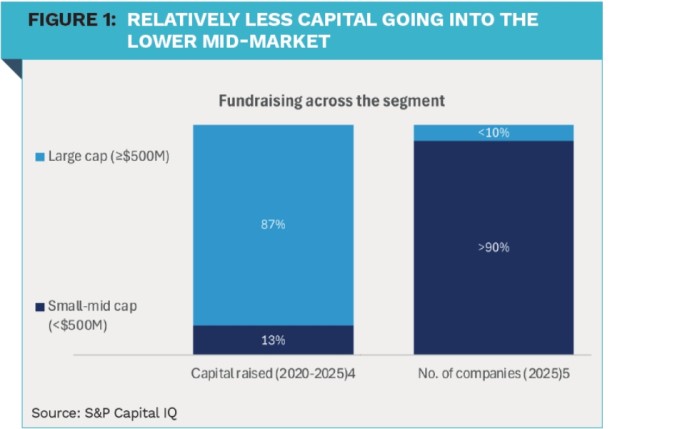

This historic focus on larger deals has created an industry imbalance, resulting in less capital chasing highly attractive opportunities in the lower mid-market. As Figure 1 shows, 86% of commitments have gone to companies at the larger end of the market, providing exposure to less than 10% of available private companies. This dearth of capital at the smaller end has increased inefficiency in the space and reduced competition for acquiring these fast-growing companies. This is evidenced by a 2.9x3 average discount in purchase multiple in the lower mid-market.

In the 10 years that our team has specialised in this area, we have witnessed the consistent outperformance potential of lower midmarket companies. It is on the back of these dynamics that we believe investors are increasingly keen to exploit the gap between capital raised and the investment outlook. Maintaining a clear definition of what the lower mid-market is, is essential to successfully tapping into the forces driving this outperformance.

Forces of outperformance

The outperformance of lower mid-market companies is driven by a range of factors, starting with the broad and attractively valued opportunity set. Smaller companies are the backbone of the global economy, representing the vast majority of private companies. This part of the market, therefore, encompasses a broad investment universe – spanning more sectors and industries than its larger counterparts – and the potential to offer investors a broader, more diverse range of opportunities to select from. The average EBITDA multiple for deals under $ 500 million – which measures how much investors pay relative to a company’s earnings – is about 11.6x, versus 14.5x for deals over $ 500 million.3

The lower mid-market encompasses a broad investment universe and the potential to offer investors a broader, more diverse range of opportunities to select from.

A second key driver of outperformance is the lower reliance of these companies on financial engineering and debt. This allows them to be less IPO dependent and more attractive to several different types of buyers opening up a greater range of exit pathways. In the aforementioned fifth vintage2 of our co-investment program, 40% of the deals had zero debt attached to them. This is an outcome of both the nature of the sector and the specificity of our selection process and approach. We specialise in buying into already healthy businesses that can generate strong returns through operational value creation and strategic guidance. This ultimately allows us to build a portfolio of companies that we believe will be attractive to a broad range of buyers.

Although ripe with investment opportunity, the lower mid-market remains one of the hardest parts of the industry to access. Transactions often occur in a less formalised setting relative to larger deals, and many companies are taking on institutional capital for the first time. Due to their size, target companies are likely to have less established due diligence processes, reporting and governance structures.

Given the less-formal nature of the market, the task of constructing a lower midmarket portfolio can be challenging, requiring specialised knowledge and an established network. As a result, prospective investors must approach the lower mid-market with a clear definition, dedicated resource and the experience and expertise to help these companies deliver on their high-return potentials.

|

SUMMARY The term ‘lower midmarket’ describes a vast and undefined investment segment, but the parameters of the universe may shift depending on which investor you talk to and what they might be selling. Lower mid-market companies with an enterprise value up to $ 500 million tend to outperform due to attractive valuations, operational value creation and diversified exit options, despite limited accessibility. The industry’s historic focus on larger deals has created an imbalance in the market whereby less capital is chasing highly attractive lower mid-market opportunities. |

- Source: Bain & Company — Global Private Equity Report 2025.

- The investment period for this fund ended on 30 June 2025 - it is no longer accepting new investors.

- Source: PitchBook data for North America and Europe across 2019-2024. EV/EBITDA multiples weighted by deal count per year. Lower mid-market is defined as transactions with enterprise value (EV) below $500m, while Large and mega market refers to transactions with EV of $500m and above.

- 2020-2025 US and Europe fundraising data from PitchBook’s Annual 2025 European and US Private Equity Breakdown reports. All underlying fundraising figures are reported in USD.

- Source: S&P Capital IQ, covering commercially- active US businesses as of 13 February 2025. Target companies are defined as those with revenues between $10m-$250m, which are considered representative of our invest- ment opportunity. Non-target companies are those with revenues greater than $250m.

Read the full report in Financial Investigator magazine