Annebeth Roor: From relative SAA optimisation to target-based investing

This article was originally written in Dutch. This is an English translation

Strategic asset allocation (SAA) is the cornerstone of any investment process. But is the traditional SAA framework still sufficient in a changing and uncertain world? Three researchers from Erasmus University present an integrated alternative.

By Annebeth Roor-Wubs, Dirk Schoenmaker and Karen Maas

For institutional investors, the SAA is the starting point of the investment process, where macroeconomic expectations are used to determine how a portfolio will be allocated across asset classes, with the aim of achieving an optimal balance between risk and return. However, this traditional framework does not provide sufficient scope to assess the impacts of transitions. For example, what are the effects of climate change, social inequality, resource scarcity and geopolitical tensions on the portfolio? We present an alternative SAA framework in which these developments are integrated.

Sustainable investing has long been practised within asset classes, but integration at the SAA level lags behind. This represents a missed opportunity and a risk. Developments such as the energy transition, an ageing population or trade fragmentation influence sectors and, consequently, inflation, interest rates and growth. Institutional investors who do not factor these developments into their asset allocation policy run the risk of being ill-prepared for structural changes.

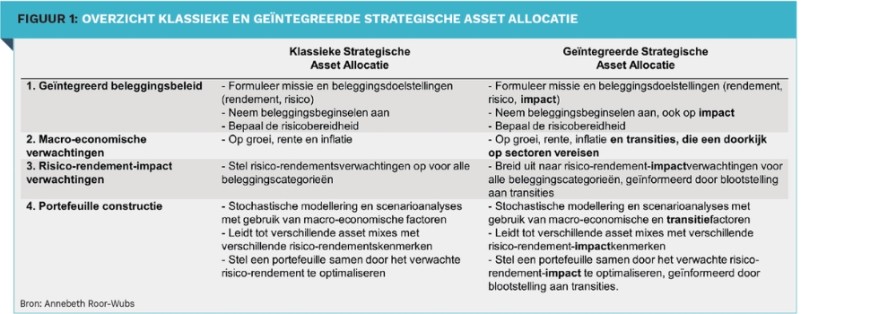

Four steps towards an integrated framework

The framework we propose adds two dimensions to traditional risk-return thinking: transitions and impact. This is achieved in four steps.

- 1) Integrated investment policy

The foundation is an investment policy in which social objectives are embedded alongside financial goals. For example, an investor may incorporate objectives such as combating environmental damage, reducing social inequalities, or mitigating strategic dependencies in the areas of energy and critical raw materials.

- 2) Macroeconomic expectations including transitions

Transitions are treated as structural macroeconomic variables rather than external risk factors. The energy transition, protein transition, ageing population and trade fragmentation thus become part of richer and more realistic scenario analyses.

- 3) Risk-return-impact expectations

For each asset class, the analysis considers not only risk and return, but also the expected impact and exposure to transitions. An analysis at country and sector level highlights where the vulnerabilities lie.

- 4) Portfolio construction

The final allocation is based on an integrated assessment of risk, return and impact. This may lead to different allocation choices, such as a greater emphasis on infrastructure, local markets, or sectors that contribute to biodiversity conservation. The result is a portfolio that is financially and socially robust and better able to withstand structural uncertainty.

Investors are not mere spectators

A key insight of this alternative integrated framework is that investors are not merely exposed to transitions, but also actively influence them. Through capital allocation, active shareholding and systemic influence, institutional investors help to steer the direction and pace of economic and social transformations.

Transitions are not linear, but often occur in fits and starts, whether or not as a result of natural disasters, changes in government policy or geopolitical developments. During transitions, new business models must be supported. Established companies face the challenge of adapting to change, whilst some companies resist it.

Investments in renewable energy, new technology, affordable housing or local production capacity can accelerate transitions and strengthen the strategic autonomy of economies. By limiting investments to established companies, investors can slow down transitions, as they have a vested interest in maintaining the status quo.

By taking the impact of investments into account, impact is no longer a by-product but an integral part of the investment decision. The role of the institutional investor thus shifts from that of a passive risk manager to an active participant in economic transformation.

Measuring what really matters

A key practical challenge is the nature of the sustainability data available. ESG scores are relative in nature: they show how a company compares with its sector peers, but not whether the company is actually contributing to a more sustainable economy. Sustainability research has identified limits for the environment and nature – known as ‘planetary boundaries’ – within which we as humanity can coexist in a healthy way. These system boundaries provide an objective basis for determining whether companies are sustainable. For example, CO₂ emissions can be measured against climate targets.

Social objectives are more challenging, as they are partly culturally determined and linked to national laws and regulations. Nevertheless, a basis can be found in internationally accepted standards against which social indicators can be assessed. Consider, for example, the payment of a living wage to all employees.

This approach to measurement aligns with Stephen Covey’s principle: begin with the end in mind. Anyone wishing to know whether a portfolio contributes to a sustainable economy must measure it against that ultimate goal, not against the least bad competitor.

Practical implications for investment professionals

The integrated SAA framework breaks with the common practice of treating impact as a separate investment category. This risks investors narrowing the discussion down to just a small part of the portfolio. By explicitly incorporating transitions and impact into allocation decisions, across all asset classes, a more coherent and future-proof investment process is created.

This requires new data, scenarios and analytical methods. However, the transition does not have to happen all at once: a combination of incremental improvements and parallel innovations enables a phased implementation. For investment professionals, the framework offers concrete tools to better position portfolios in the face of structural uncertainty, geopolitical risks and societal transitions.

A necessary evolution

In a world where economic efficiency is increasingly weighed against strategic autonomy and stability, an integrated approach to SAA is no longer a luxury. By considering risk, return and impact together, institutional investors can not only respond more effectively to a changing world, but also actively contribute to an economy that is sustainable and resilient. That is the essence of what we are advocating: a fundamental rethink of how we approach and practise strategic investment.

|

IN SHORT A new SAA framework must integrate risk, return and social impact. Transitions such as climate change and geopolitical shifts deserve explicit consideration in scenarios and allocation decisions. Institutional investors drive transitions through capital allocation, active shareholding and systemic influence. Integrated SAA makes sustainable investing more targeted and future-proof. |

Read the article in the digital magazine